Global Reporting Initiative (GRI) was formed in 1997 with the support of the United Nations Environment Programme (UNEP). Since 1997, GRI’s publications have become the most widely used sustainability reporting standards. Any organization, large or small, public or private, from any sector or location, can use the GRI Standards. Reports aligned with these standards are drawn upon by reporters, stakeholders, and other users.

GRI Framework Overview

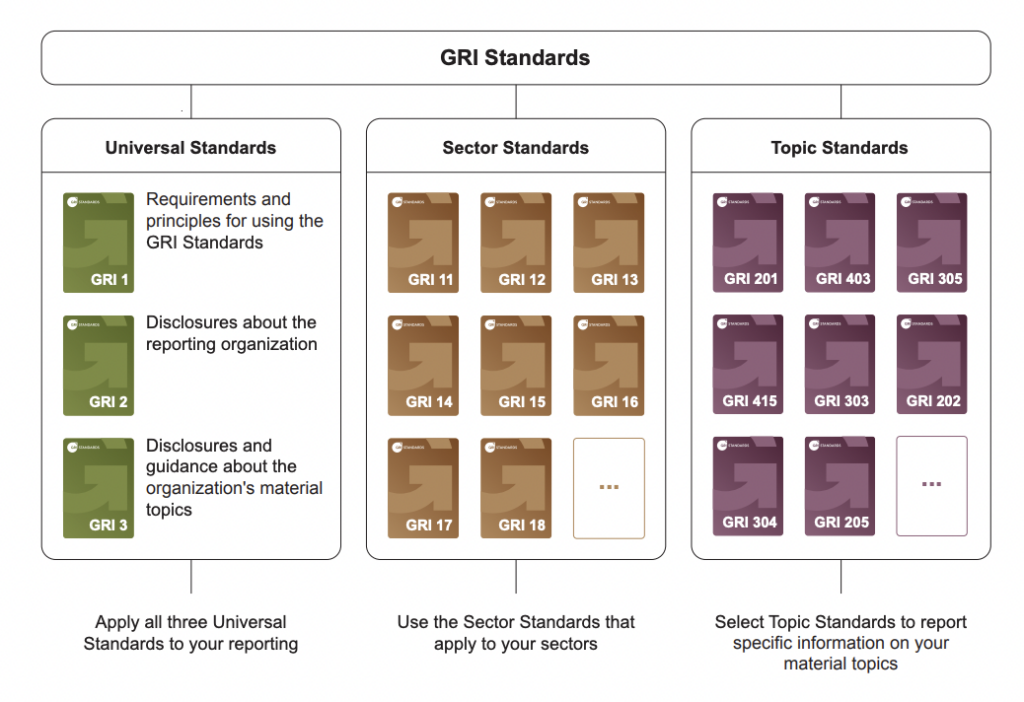

The GRI Standards are comprised of three series of standards that complement each other:

- GRI Universal Standards (GRI 1-3)

- GRI Sector Standards (GRI 11-99)

- GRI Topic Standards (GRI 201-418)

The GRI Universal Standards list the requirements to report in accordance with GRI requirements. Within the Universal Standards cover general business disclosures as well as guidance on how to determine topic materiality.

The GRI Sector Standards are intended to increase the quality of reporting by organizing requirements within specific industries. These standards are in continual development and will be developed for 40 sectors in total. So far, 3 of these sector standards have been finalized for industries with the highest impact – Oil & Gas, Coal, and Agriculture, Aquaculture, and Fishing. The Sector Standards direct specific industries to topics that are likely material and to the specific Topic Standards that apply to an industry.

The GRI Topic Standards cover the requirements for disclosure related to specific subjects like water consumption or waste generation. These standards are where the most familiar environmental, social, and governance (ESG) disclosures are described. These range from environmental (GRI 301-308) to labor (GRI 401-409) related topics. Companies without specific Sector Standards should first identify material topics before determining which Topic Standards are most applicable.

Conforming with GRI Standards

The GRI Standards are open source and free to use in disclosure reporting. Most organizations that use the GRI Standards do so when developing their annual sustainability reports. By disclosing their ESG reports, companies benefit by improving transparency with stakeholders and allowing for meaningful benchmarking to be done among industry peers.

GRI provides two tiers of reporting compliance: reporting in accordance with or with reference to GRI Standards.

Reporting in Accordance with GRI Standards

To report in accordance with the GRI Standards, an organization must fulfill all nine requirements set out in section 3 of GRI 1:

- Requirement 1: Apply the reporting principles

- Requirement 2: Report the disclosures in GRI 2: General Disclosures

- Requirement 3: Determine material topics

- Requirement 4: Report the disclosures in GRI 3: Material Topics

- Requirement 5: Report disclosures from the GRI Topic standards for each material topic

- Requirement 6: Provide reasons for omission for disclosures and requirements that the organization cannot comply with

- Requirement 7: Publish a GRI content index

- Requirement 8: Provide a statement of use

- Requirement 9: Notify GRI

Reporting with Reference to GRI Standards

If your organization is unable to comply with the 9 requirements to be in accordance with the standards, it can “Report with Reference to the GRI Standards” by following these three requirements:

- Publish a GRI content index

- Provide a statement of use

- Notify GRI

Take Action

Is your organization ready to get started reporting to the GRI? Interested in streamlining the quantitative data management to support your GRI reporting? Our sustainability consultants would love to help you on your way! Reach out to our team for an initial discussion.